Home Insurance in Los Angeles: What Buyers and Homeowners Need to Know

Buying a home is one of the largest financial commitments most people will ever make, and homeowners insurance plays a critical role in protecting that investment. Think of it as a financial safety net designed to step in when the unexpected happens.

Homeowners insurance generally helps in three key ways:

It covers repair and rebuilding costs.

If your home is damaged by events such as fire, severe weather, or other covered losses, insurance can help pay for repairs, and in serious cases, the cost to rebuild the home.

It protects your personal belongings.

Your policy typically extends beyond the structure itself to cover items inside the home, including furniture, electronics, clothing, and other personal property if they’re stolen or damaged.

It provides liability protection.

If someone is injured on your property, homeowners insurance can help cover medical expenses and, if necessary, legal costs, offering important protection against potentially significant financial exposure.

Home insurance has become one of the biggest surprise costs for Los Angeles buyers and homeowners. Many people searching online right now are asking the same questions: How much is home insurance in LA? Why are rates going up so fast? Will I even be able to get coverage?

Here’s what’s really happening and what to plan for if you’re buying or owning a home in Los Angeles.

Why Are Home Insurance Premiums Increasing?

Home insurance costs are rising for several reasons, but the main drivers are tied to growing risk and higher rebuilding expenses. According to the Insurance Research Council (IRC), insurers are facing more frequent and severe weather-related losses than in the past.

As storms, wildfires, and other natural disasters become more common, insurance claims increase. At the same time, the cost of construction materials and labor continues to rise. This means that repairing or rebuilding damaged homes is significantly more expensive, and those higher costs are reflected in today’s insurance premiums.

How much is home insurance in Los Angeles right now?

Urban LA neighborhoods (flat areas, no nearby brush):

Expect roughly $2,000–$3,500 per year for a typical single-family home.Hillside, canyon, or brush-adjacent areas:

Premiums often land between $3,500–$6,500+ per year, depending on fire risk, home age, and rebuild cost.Higher-risk areas using the California FAIR Plan:

Many homeowners pay $5,000–$7,000+ per year when combining:a FAIR Plan fire policy

plus a separate companion or wrap policy for non-fire coverage

Actual pricing depends heavily on location, rebuild cost, and carrier availability, not just home value.

Why are Los Angeles home insurance rates increasing so much?

Wildfire risk is now priced year-round

Los Angeles is no longer viewed as a seasonal fire market. Insurers are pricing in:

year-round wildfire risk

wind-driven fires

post-fire mudslides and flooding

Even homes that have never had a claim are affected if they’re near hills, canyons, or vegetation.

Rebuilding a home in LA costs far more than before

Insurance is based on rebuild cost, not market value. In Los Angeles:

labor is more expensive

materials cost more

permitting and code upgrades add significant cost

Higher rebuild estimates automatically push premiums higher.

Fewer insurance companies are writing new policies

When fewer carriers compete, prices rise. Some companies now:

limit new business

non-renew policies in higher-risk zones

require stricter underwriting standards

New California pricing rules changed the math

California now allows insurers to:

use forward-looking wildfire models

pass through more reinsurance costs

This keeps insurers in the state, but it also means larger and faster rate increases than homeowners saw in the past.

What is the California FAIR Plan and why are people using it?

The FAIR Plan is California’s last-resort fire insurance. It:

covers fire and smoke damage only

does not include theft, liability, or water damage

Most homeowners using FAIR Plan must also buy a companion policy, which is why total costs can jump significantly.

FAIR Plan usage has increased sharply across LA County, especially in hillside and canyon neighborhoods.

Can home insurance affect buying a home in Los Angeles?

When should you start homeowners insurance when buying a house?

You should begin shopping for homeowners insurance as soon as escrow opens, not at the end of the transaction.

Most lenders require proof of insurance before they will fund the loan, and waiting too long can delay closing.

What is the 80% rule in homeowners insurance in Los Angeles?

The 80% rule means you should insure your home for at least 80% of its replacement cost—the cost to rebuild it, not its market value.

If your coverage is below that level, insurers may reduce how much they pay on partial losses, even if the damage is far less than your policy limit.

Example:

If your home would cost $1,000,000 to rebuild, you should carry at least $800,000 in dwelling coverage.

If you only insure it for $600,000 and suffer a $200,000 loss, the insurer may pay only about 75% of the claim (around $150,000, minus your deductible).

Why this matters in Los Angeles: Rebuilding costs in LA are high and rising, making underinsurance more common than people realize. Updating your dwelling coverage after remodels or cost increases helps you stay above the 80% threshold and avoid reduced claim payouts.

Can you buy a house in Los Angeles without homeowners insurance?

Yes, but only if you are paying all cash.

California law does not require homeowners insurance to legally own a home in Los Angeles.

Mortgage lenders do require insurance. If you finance the purchase, homeowners insurance is mandatory to protect the lender’s collateral.

Cash buyers are not legally required to carry insurance. If there is no lender involved, you may choose to go without it without violating any state or local law.

Common Home Insurance Issues During Escrow in Los Angeles

Insurance approval can delay or derail escrow.

Most lenders require proof of homeowners insurance before funding the loan. If coverage isn’t secured in time, escrow can be delayed or even fall apart.

High-risk LA areas create coverage challenges.

In hillside, canyon, or brush-adjacent neighborhoods, standard insurers may decline coverage or offer very high premiums. This can impact a buyer’s debt-to-income ratio and jeopardize loan approval.

FAIR Plan policies add complexity.

Some properties require a California FAIR Plan fire policy plus a separate companion policy for liability and other risks. Coordinating multiple policies can take extra time during escrow.

Escrow Accounts, Premiums, and Cash to Close

If your loan includes an impound account, the lender will collect estimated insurance premiums at closing, plus a reserve. This can significantly increase the cash required to close.

Last-minute premium changes may trigger escrow recalculations, higher monthly payments, or even new loan disclosures.

Inspection-Related Insurance Issues

Insurance carriers may require repairs, such as roof work, electrical updates, plumbing fixes, or brush clearance—before issuing or continuing coverage. If discovered late in escrow, buyers may need to negotiate repairs or credits quickly.

Some policies limit coverage for older roofs, unpermitted additions, or certain plumbing types, which can affect a buyer’s willingness to proceed.

Wildfire Risk Considerations

In designated wildfire zones, insurers may impose higher deductibles, surcharges, or non-renewal risks. Buyers should confirm insurability and cost early, before removing contingencies.

Recent California laws also affect how wildfire insurance claims and escrowed insurance funds are handled, which may be relevant for properties with past or future fire exposure.

Practical Steps for Buyers

Secure insurance quotes immediately after offer acceptance, not at the end of escrow.

Review projected insurance impounds with your lender so you understand both cash to close and your true monthly payment.

For hillside or brush-area properties, ask upfront whether FAIR Plan coverage has been required in the neighborhood.

Key things buyers need to know:

Lenders require insurance before closing

Insurance quotes should be obtained early in escrow

Some homes are insurable only through FAIR Plan

Insurance availability can influence:

whether a deal closes

monthly ownership costs

long-term affordability

How can homeowners reduce insurance costs in LA?

Practical strategies that actually help:

Shop aggressively: Independent brokers often access carriers you won’t find online.

Increase deductibles: Especially for fire coverage.

Home hardening: Non-combustible roofs, cleared defensible space, enclosed eaves, ember-resistant vents.

Bundling: Auto + home can still produce savings with some carriers.

Claims history review: Even small prior claims can raise rates, avoid filing minor claims.

In higher-risk areas, documented wildfire-mitigation work can meaningfully reduce premiums.

How much is homeowners insurance on a $1,000,000 house in California?

There isn’t a single fixed rate, but most estimates show that insuring a home with approximately $1 million in dwelling coverage in California can cost several thousand dollars per year. Actual premiums vary widely depending on location, fire risk, coverage limits, deductible, and insurer.

Typical cost ranges you may see:

Californians with a $1 M dwelling coverage policy might pay around $4,800–$5,000 annually (~$400 +/month) — based on data for Los Angeles-area costs at that coverage level.

National estimates for a $1 M home (not California-specific) put the average around about $7,400/year for $1M dwelling coverage in the U.S. — but local conditions and risks shape your actual CA rate.

What buyers and homeowners should plan for going forward

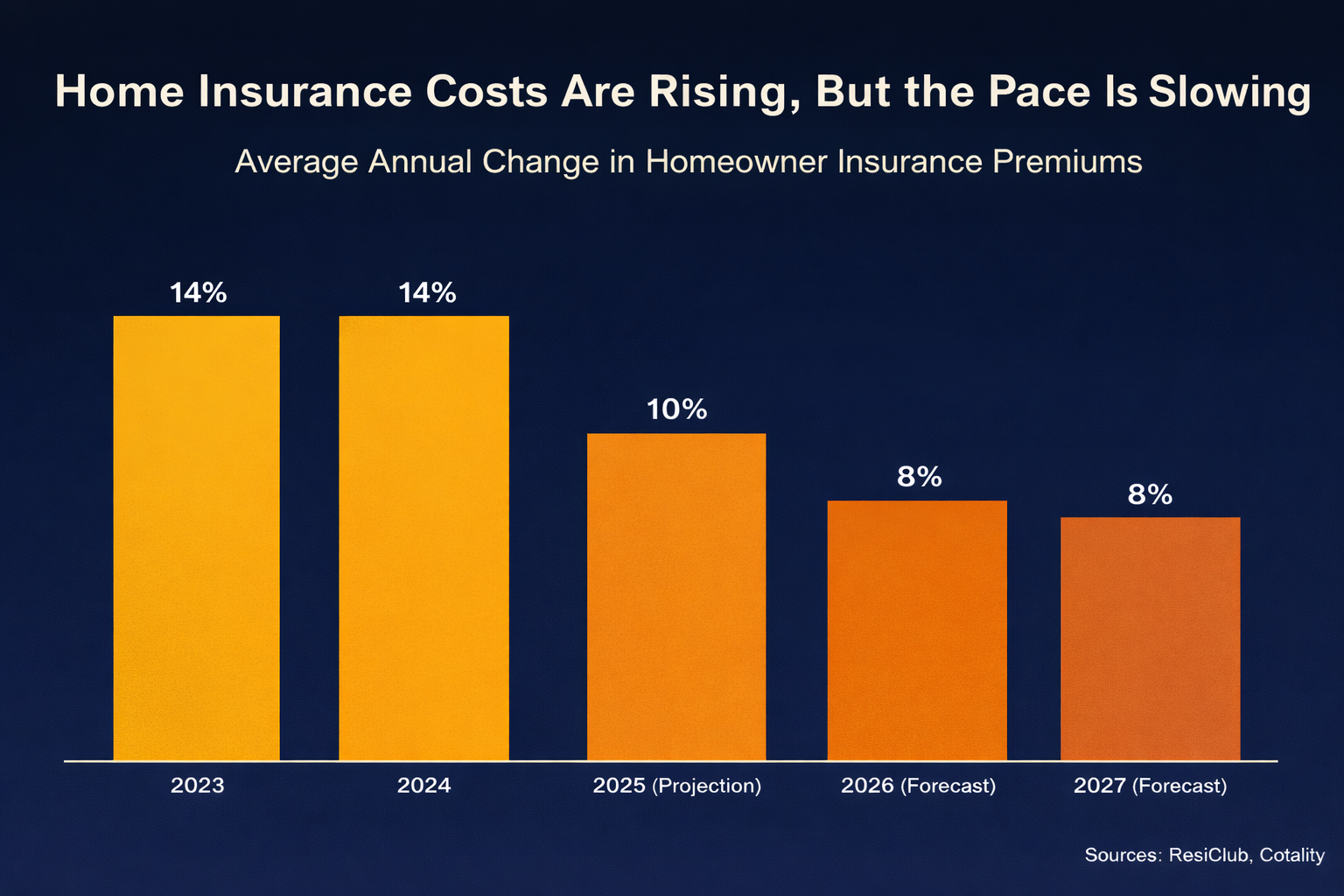

Many LA homeowners will pay 30–50% more in 2025–2026 than they did in 2023.

Rates are unlikely to return to pre-2020 levels.

Insurance costs should be treated as a core ownership expense, not an afterthought.

What homeowners insurance does NOT cover in California

Standard homeowners insurance in California excludes several major risks, along with anything specifically listed in your policy’s exclusions.

Common exclusions include:

Earthquakes and earth movement: Damage from earthquakes, landslides, mudslides, or ground movement is not covered and requires a separate earthquake policy, often through the California Earthquake Authority.

Flooding from outside water: Overland flooding from storms, rivers, or coastal surge is excluded and requires separate flood insurance.

Wear and tear or maintenance issues: Aging roofs, rot, corrosion, settling, and general deterioration are not covered.

Water- and mold-related limits:

Long-term leaks or seepage are typically excluded; coverage applies only to sudden and accidental water damage.

Mold and mildew are often excluded or capped at low limits.

Sewer or drain backups usually require a specific endorsement.

Liability and use exclusions:

Business use of the home is limited unless a business endorsement is added.

Intentional or criminal acts are never covered.

Certain dog breeds or high-risk features (such as some pools or trampolines) may be excluded without special endorsements.

Other standard exclusions:

War, nuclear events, and government action

Additional damage caused by neglect after a loss

California-specific note:

Wildfire damage is generally covered under standard homeowners policies, but coverage limits and disputes can arise around smoke damage, debris removal, code upgrades, and additional living expenses.

Because exclusions vary by insurer, homeowners should review their policy carefully and confirm how earthquakes, floods, water damage, and wildfire-related losses are handled under their specific coverage.

Can insurance cancel or non-renew after I buy the house?

Yes, your homeowners insurance can be canceled mid‑term in limited cases (like nonpayment, fraud, or serious hazards) and can be non‑renewed at the end of the term with advance written notice.

Does homeowners insurance cover wildfires in Los Angeles?

Yes. Standard homeowners insurance in Los Angeles covers wildfires under the fire peril, including damage to the home, personal belongings, debris removal, and additional living expenses.

What to know:

Coverage typically includes the structure, detached buildings, personal property, and temporary housing.

Some policies impose wildfire-specific deductibles (often 2–5% of the dwelling limit) or require fire-hardening measures like cleared brush or ember-resistant vents.

In higher-risk areas, some insurers have non-renewed policies, pushing homeowners to the California FAIR Plan, which covers fire only and often must be paired with a companion policy.

Related risks like post-fire mudslides or flooding are not covered and require separate insurance.

Should buyers get insurance quotes before making an offer?

Yes. Los Angeles buyers should get preliminary homeowners insurance quotes before making an offer, especially in higher fire-risk areas where coverage can be limited or expensive.

Why this matters:

Some hillside or brush-area homes can’t get standard insurance and may require a FAIR Plan fire policy plus a companion policy, which can impact affordability and loan approval.

Insurance premiums vary widely by ZIP code, and late surprises can delay escrow or force buyers to cancel.

Best practice:

Run quotes as soon as you identify serious target properties using the address.

Share estimated insurance costs with your agent so they can guide you toward insurable, financeable homes.

Bottom Line for Los Angeles Buyers and Homeowners

Homeowners insurance in Los Angeles is no longer a simple checkbox at the end of the buying process. Between rising premiums, wildfire risk, tighter underwriting, and the growing use of the California FAIR Plan, insurance has become a strategic part of owning and purchasing property.

The key is planning ahead. Understanding your risk zone, getting insurance quotes early, and knowing how coverage impacts escrow, monthly payments, and long-term affordability can prevent costly surprises and protect your investment.

Whether you’re buying your first home, moving up, or purchasing in a hillside or brush-area neighborhood, treating insurance as a core ownership expense, not an after thought , will put you in a far stronger position to close smoothly and own with confidence.